The article is co-authored by Nadine Esposito, CEO and founder of Wellthspan Advisory.

As longevity has risen, a mere focus on lifespan is no longer enough to age sustainably. We need to reposition our focus to healthspan as well as wealthspan to shape the extra years as opportunity instead of strain. Using a simple 5+1 framework from Wellthspan Advisory to keep the whole life in focus, we can make small moves today to make longer lives work significantly better for families, employees, and customers.

We are quietly moving into a world of 90- and 100-year lives, while most of the systems that carry us through adulthood were built for lives that ended twenty to thirty years earlier. Counting years lived is no longer enough; what matters is how long people remain healthy and financially in control, and how long they can rely on the systems around them without becoming a burden on themselves or others.

For households, employers, and financial institutions, the real ‘longevity challenge’ is to maximise the years we spend in good health and financial security while shrinking the period of dependency and strain at the end of life.

A life you might recognise

She is in her mid-forties. She enjoys her work, exercises regularly, and is careful with money. Her grandmother hoped to see seventy. Her mother reached her late seventies and now needs help with everyday life. She herself may well live into her nineties.

When she looks ahead, she does not see a straight line. Career programmes around her still assume a peak in the early fifties and a smooth glide into retirement. Pension rules and products are calibrated for short drawdowns, not three or four decades of post-work life. Health insurance pays generously for treatment but offers much less for prevention, mental health, or sustained resilience. Financial advice tends to project today’s household into the future as if it will stay stable, although she knows that careers, relationships, health, and responsibilities will change. Her family is spread across cities. The house she loves may one day be difficult to navigate.

She has not failed. The systems around her were designed for the lives her parents lived, not for the life she is likely to live.

How we gained years – and why they feel fragile

The extra decades were not won by miracle anti-ageing drugs. They came from basic progress: clean water and sanitation, vaccines and antibiotics, safer roads and workplaces, better care for mothers and infants. People now survive childhood and midlife and reach older ages in far greater numbers. This ageing success is real. But the redesign of the system to handle ageing sustainably has not kept up.

As longevity increased, it has become clear that measuring only the number of years lived is insufficient to describe lived reality. Two people may live to the same age yet experience those lived years in profoundly different ways.

This recognition has led to two additional concepts, beyond lifespan, that approach ageing more holistically:

Healthspan measures the years lived in good physical, mental, and cognitive health – the years in which people can live independently, work if they want to, make decisions, and enjoy relationships.

Wealthspan measures the years in which financial resources translate into genuine choice: when there is enough income and liquidity at the right time, and enough cognitive capacity and support to manage complexity.

A long life without health or financial agency does not feel like success; it is an extended period of exposure to risk and dependency.

Six everyday gaps in longer lives

Longer lives and older systems create tension which shows up in ordinary decisions rather than in abstract debates.

Six gaps are particularly visible:

Medicine built for cure, not prevention. Health systems excel at acute care, yet the conditions that shape later life – chronic disease, mental health challenges, cognitive decline – unfold over years. Prevention and early detection pay off, but incentives still favour treatment once something has gone wrong, and few people have protected time for health.

Wealth planning for short retirements, not uneven complexity. Traditional plans imagine continuous careers and a brief drawdown. Real lives are more uneven: careers shift, caregiving interrupts earnings, health events arrive unexpectedly, and retirements can last for decades. Wealthspan depends on income timing, liquidity, and resilience – and on the ability to make good decisions as life becomes more complex.

Work organised for continuity, not reskilling. A degree at twenty will not carry someone through fifty or sixty working years. Skills expire, new roles emerge, and phases of recovery or caregiving create gaps. Many career ladders and pension rules still penalise interruption, even though longer lives require explicit paths for reskilling and more flexible ways of working.

Family care assuming proximity, not fragmentation. Care systems still rely heavily on families to provide coordination, supervision, and everyday support. Yet families are smaller, more geographically dispersed, and often stretched by work and childcare of their own. Many people live alone for long stretches of adulthood, while caregiving responsibilities arrive later, last longer, and are harder to combine with paid work. When care needs increase, support is often fragmented and uneven, shaped more by who happens to be nearby than by what is actually needed.

Housing designed for shorter occupancy, not prolonged living. Most homes were not built for changed mobility or cognition. Stairs become barriers, bathrooms turn into risk zones, and isolation grows when driving is no longer safe and neighbours move away. Moving late in life is difficult and often happens in a rush after a health event, yet housing is also the main store of wealth for many families. That creates a constant trade-off between place, safety, and liquidity.

Care risk: the gap between planning and availability. Most longevity planning assumes that if care is financially secured, it will be accessible when needed. But care risk challenges that assumption. With growing demand and persistent care workforce shortages, having the means to pay for care no longer automatically guarantees access to it. A person may have planned carefully, set aside the funds, even identified providers in advance – and still find that when care is needed, capacity simply is not there. Care risk is not primarily a financial failure. It is a supply and coordination failure that no amount of financial planning can fully hedge against.

Over longer lives, these gaps compound. A health issue at fifty influences earnings at fifty-five, savings at sixty, care options at seventy, and housing decisions at eighty.

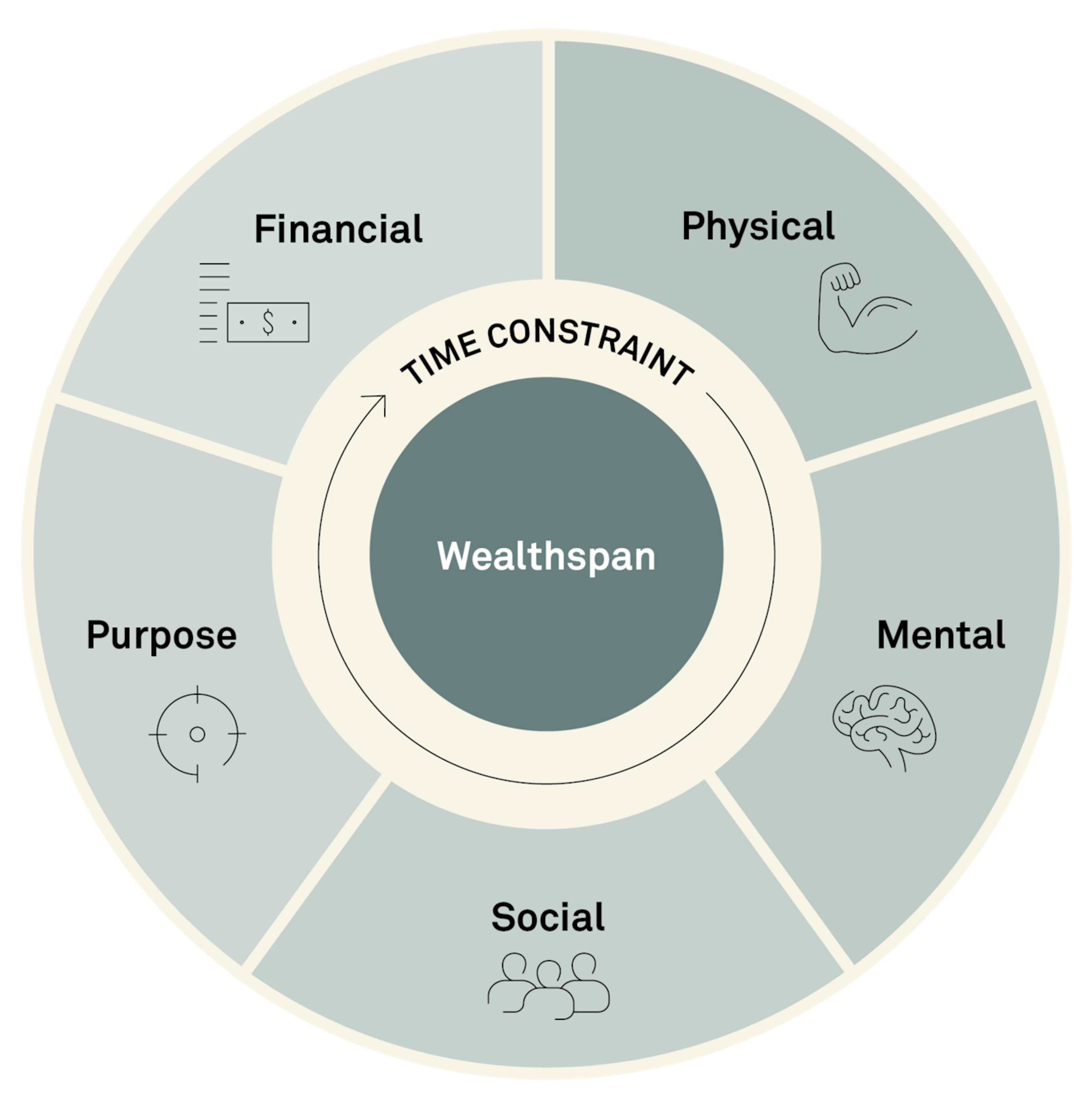

A simple way to see the whole life

Single fixes tend to disappoint because they ignore the wider picture. A simple way that households, employers, and financial institutions can hold this wider picture is to use the 5+1 framework, developed by Nadine Esposito, Founder of Wellthspan Advisory.